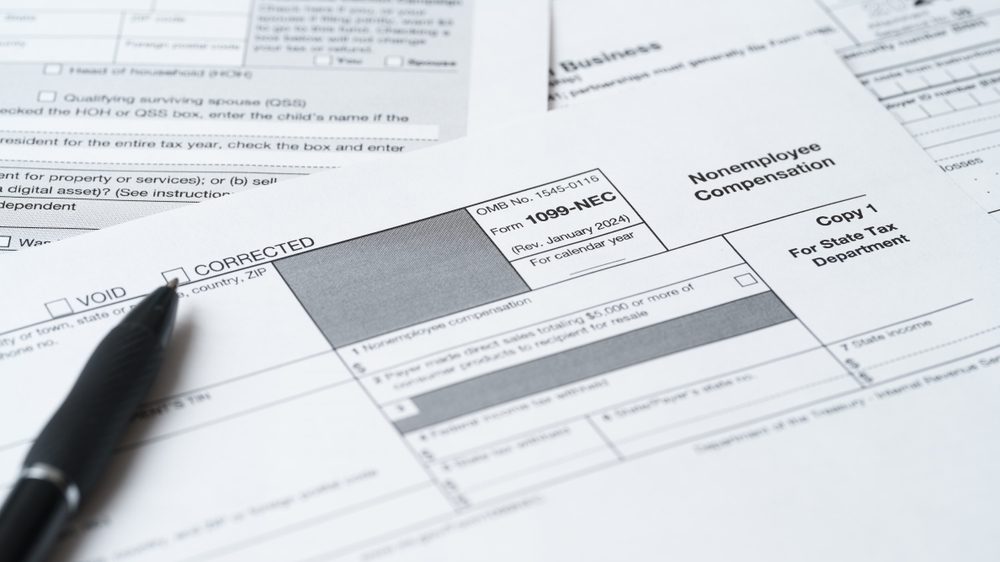

For small business owners, understanding 1099 compliance is essential to staying compliant with IRS regulations and avoiding costly penalties. Whenever a business hires independent contractors, freelancers, or service providers, it may be required to issue Form 1099-NEC to report payments made throughout the year. While the process may seem simple, rules around classification, documentation, and deadlines make it important to stay organized and accurate.

Understanding Worker Classification: Employee vs. Independent Contractor

One of the most important steps in 1099 compliance is correctly classifying workers as either employees or independent contractors. Misclassification can result in tax penalties and back taxes. The IRS evaluates factors such as behavioral control, financial control, and the overall relationship to determine classification. Proper classification ensures businesses report payments correctly and avoid payroll tax issues.

Collecting W-9 Forms and Filing 1099-NEC Correctly

Before paying contractors, businesses should collect a completed Form W-9 to obtain accurate taxpayer information. This is necessary for preparing year-end 1099-NEC forms for contractors paid $600 or more. Without proper documentation, businesses may face filing delays or backup withholding requirements. Staying organized with contractor records throughout the year helps ensure accurate and timely reporting.

Filing Deadlines, Penalties, and Staying Compliant Year-Round

Timely filing is critical for 1099 compliance. Businesses must submit 1099-NEC forms to contractors and the IRS by January 31 each year. Late filings can result in penalties that increase the longer the forms are delayed. Maintaining consistent bookkeeping and tracking contractor payments throughout the year helps reduce stress and ensures compliance during tax season.

Conclusion

In conclusion, 1099 compliance is a key responsibility for small business owners working with independent contractors. From proper classification to collecting W-9 forms and meeting filing deadlines, each step helps ensure IRS compliance and avoid penalties. For professional assistance with 1099 filing, tax planning, or small business accounting, contact MARIELA RUIZ, CPA, PLLC at (956) 997-0067 or visit our website at www.mruiz-cpa.com to keep your business compliant and financially organized year-round.